Mastering DCF Analysis: A Comprehensive Guide

In the ever-evolving world of finance and investment, understanding how to value an asset is crucial. One of the most reliable and insightful methods used by financial analysts is the Discounted Cash Flow (DCF) analysis. Whether you’re an aspiring investor, a student of finance, or a seasoned professional, mastering DCF analysis can provide you with a significant edge in making informed financial decisions.

Despite its complexity, DCF analysis is a powerful tool that helps in evaluating the intrinsic value of an investment based on its expected future cash flows. By meticulously projecting these cash flows and discounting them to their present value using an appropriate rate, analysts can determine whether an asset is undervalued or overvalued in the market.

This comprehensive guide aims to demystify the intricacies of DCF analysis. We will explore its core concepts, trace its historical evolution, and break down its various components. Our step-by-step process will walk you through the calculation of these future cash flows, providing a framework that bridges theoretical knowledge with practical application. Furthermore, we’ll delve into the strengths and weaknesses of DCF analysis, offering strategies to enhance its accuracy. Ultimately, readers will uncover the real-world applications of DCF, seeing how it plays a pivotal role in valuing businesses and guiding investment decisions. Join us as we embark on a journey to master DCF analysis—equipping you with the skills to make more precise, value-driven financial assessments.

Understanding Discounted Cash Flow (DCF)

The Concept of DCF

Discounted Cash Flow (DCF) is a valuation method used to estimate the value of an investment based on its expected future cash flows. By predicting the actual cash you expect to generate in the future and discounting these figures back to their present value, DCF provides a more accurate assessment of a business’s value. The core idea is that a dollar today is worth more than a dollar in the future, due to the potential earning capacity. This principle is what makes DCF analysis such a powerful tool for investors and financial analysts alike.

Historical Context and Evolution

The DCF method has its roots in economic theory from the early 20th century. It gained widespread acceptance during the latter half of the century as financial markets became more complex and the need for accurate valuation methods increased. The evolution of DCF analysis reflects improvements in computing technology and an enhanced understanding of financial projections, allowing for more sophisticated models. Today, DCF is a staple in finance, serving as a critical tool in various applications, from assessing company value to driving investment decisions.

In the next section, we will dive into the fundamental components that make up a DCF analysis, encompassing everything from cash flow forecasts to terminal value calculations.

Components of DCF Analysis

Cash Flows: Definition and Importance

Cash flows are the lifeblood of the DCF analysis, representing the projected amounts of cash inflow and outflow that a company anticipates over time. Accurate forecasting of cash flows is crucial, as it directly impacts the valuation outcome. Analysts typically use historical data, market trends, and industry benchmarks to estimate future cash flows. A precise cash flow estimate ensures that the DCF model reflects the true financial health and potential of the business.

Discount Rate Determination

The discount rate is a critical component in the DCF analysis as it is used to convert future cash flows into present value. It reflects the risk associated with the cash flows and the time value of money. The Weighted Average Cost of Capital (WACC) is often employed as the discount rate for DCF evaluations. Determining the appropriate discount rate involves assessing factors like interest rates, inflation, and the specific risk profile of the company or project.

Calculating Terminal Value

The terminal value represents the estimated value of a business at the end of the projection period, accounting for the bulk of the total valuation in most cases. It incorporates the assumption that the business will continue to generate cash flows indefinitely. Analysts commonly use two methods for estimating terminal value: the Perpetuity Growth Model and the Exit Multiple Approach. Both methods require careful assumptions about growth rates and market conditions to ensure a realistic valuation.

Understanding these components is essential for executing a thorough and accurate DCF analysis. With this foundation, we will now delve into the detailed step-by-step process to apply these concepts effectively in real-world scenarios.

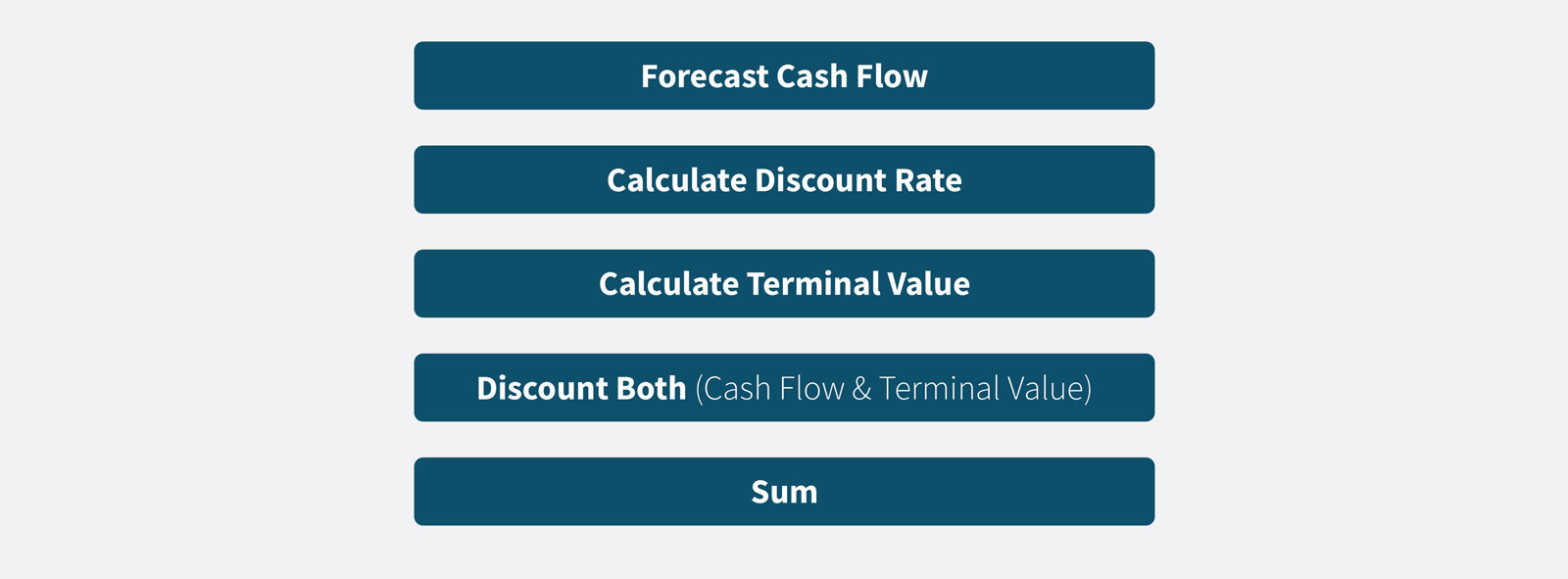

Step-by-Step DCF Analysis Process

Forecasting Cash Flows

Forecasting cash flows is the first critical step in DCF analysis. This involves estimating the future free cash flows that a company is expected to generate. Analysts typically forecast these cash flows over a period of 5 to 10 years, depending on the predictability and stability of the business operations. Accurate projections stem from a deep understanding of the business model, historical financial data, and thorough market analyses.

Applying the Discount Rate

The discount rate is used to calculate the present value of future cash flows. Choosing the right discount rate is crucial as it directly affects the valuation. Often, the Weighted Average Cost of Capital (WACC) is used as the discount rate, incorporating both the cost of equity and the cost of debt. The choice of discount rate should reflect the riskiness of the cash flows being valued.

Summing Up the Present Value

This step involves calculating the present value of forecasted cash flows and the terminal value, and summing them to determine the total present value of the business. The terminal value accounts for the value of the business beyond the explicit forecast horizon. It can be calculated using the Gordon Growth Model or an Exit Multiple approach.

By understanding and applying these steps, analysts can effectively evaluate the intrinsic value of potential investments. This detailed understanding sets the stage for analyzing the inherent advantages and limitations of DCF analysis itself, as well as exploring strategies for enhancing its accuracy.

Advantages, Drawbacks, and Mitigation Strategies

Strengths of DCF Analysis

Discounted Cash Flow (DCF) analysis offers several advantages, making it a popular method for valuing investments and businesses. One of its primary strengths is its emphasis on cash flows rather than accounting profits, providing a more accurate picture of an entity’s financial health. Moreover, DCF models are grounded in the principle of the time value of money, allowing investors to account for the value of future cash flows in today’s terms. Additionally, DCF analysis is highly adaptable and can be customized to accommodate various assumptions and scenarios, offering flexibility for users to tailor the model to specific circumstances.

Common Limitations

Despite its robustness, DCF analysis is not without its limitations. One major drawback is the model’s sensitivity to inputs and assumptions. Small changes in projected cash flows or the discount rate can significantly impact the valuation, leading to a wide range of potential outcomes. In addition, the method requires accurate long-term forecasting, which can be challenging due to economic uncertainties and market volatility. Furthermore, determining the appropriate discount rate is often subjective and can skew the results if improperly estimated.

Enhancing Accuracy in DCF

To mitigate these disadvantages, several strategies can be implemented. First, conducting thorough research and utilizing reliable data sources can improve the accuracy of cash flow forecasts. It’s also crucial to employ a range of scenarios, including best-case, worst-case, and most likely scenarios, to understand how different conditions affect valuation. Regularly updating the DCF model to reflect current market conditions and incorporating sensitivity analysis can also help in understanding the impact of changes in key assumptions. Lastly, collaborating with experts in finance or industry specialists can provide additional insights to refine the analysis.

As we delve deeper into the practical applications of DCF analysis, we can better understand its utility in valuing businesses and guiding sound investment decisions. This next section explores real-world scenarios where DCF plays a pivotal role.

Real-World Applications and Examples

DCF in Valuing Businesses

Discounted Cash Flow analysis is a critical tool for valuing businesses, particularly in mergers and acquisitions. By projecting future cash flows and discounting them to their present value, investors can determine how much a business is truly worth. For instance, in the acquisition of a tech startup, potential buyers rely heavily on DCF to understand expected future performance and decide if the asking price aligns with the return on investment. startup valuation explained

DCF for Investment Decisions

Beyond business valuation, DCF analysis is instrumental in making informed investment decisions. Portfolio managers use this method to evaluate the potential returns of stocks, real estate, or other assets. For example, in evaluating a commercial property investment, an analyst might use DCF to project rental income, applying a discount rate that reflects the risks and returns specific to that location and market. This allows investors to compare potential investments on a level playing field and choose assets that align with their financial goals.

As we delve deeper into the intricacies of DCF, understanding both sides of its impact on financial strategy will lead us to explore the advantages, drawbacks, and potential mitigation strategies involved in its application.