Debt vs Equity Financing: Choosing the Right Path for Your Business

Every business, whether it’s a small startup or an established company, comes to a crossroads: how to raise the money needed to grow. The choice usually boils down to debt financing or equity financing. Last year, over 65% of small businesses in the U.S. used some form of external financing, and deciding on the right path can shape the future of the business. This decision isn’t just about getting enough cash—it’s about how much control you want to keep, how much risk you can handle, and how you envision the future of your business. If you’re feeling unsure about which funding option makes sense for your situation, you’re not alone. Let’s break down the key differences between debt and equity financing, so you can make a decision that truly fits your business goals and values.

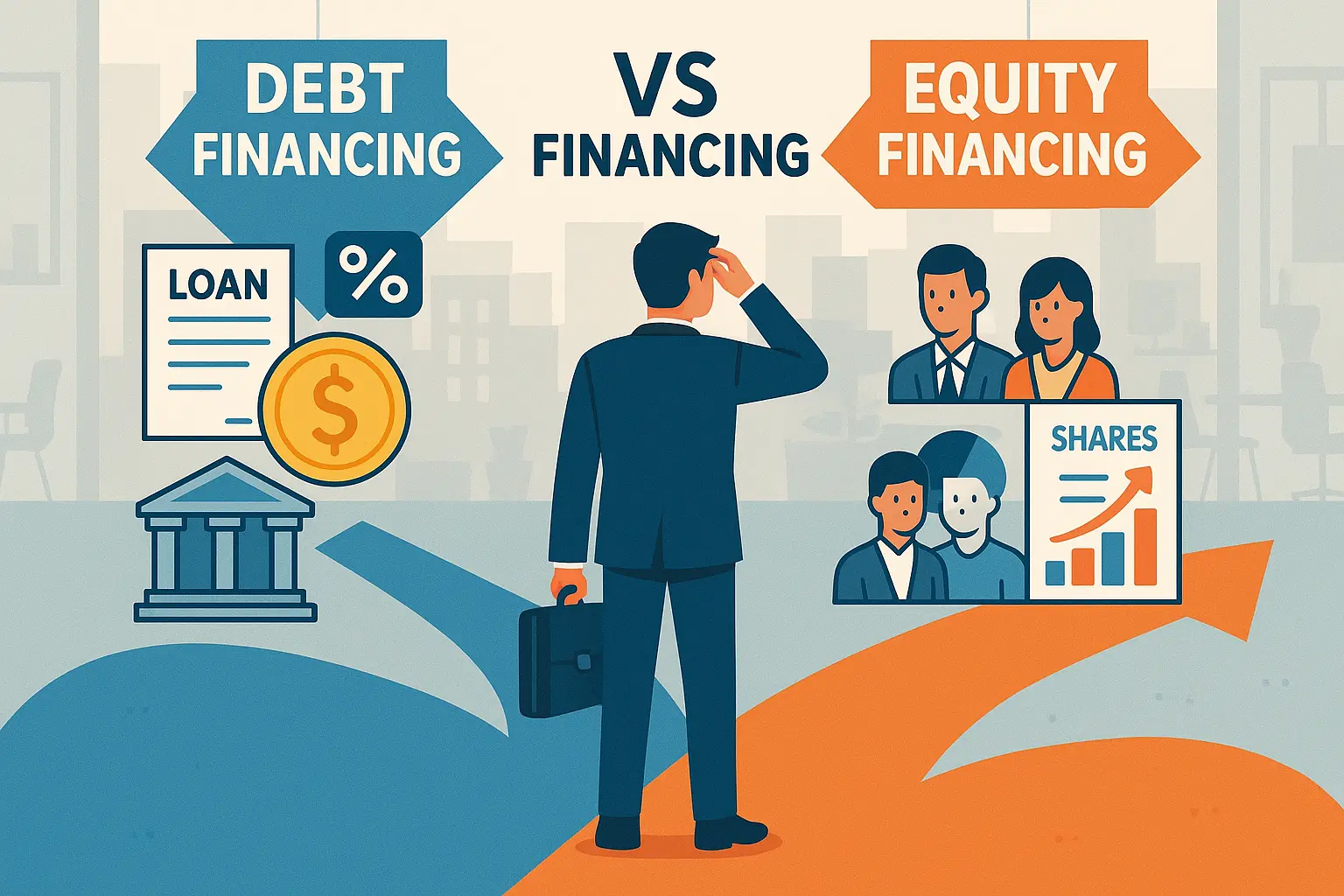

Defining Debt and Equity Financing

What is Debt Financing?

Debt financing means borrowing money with a clear promise to pay it back, usually with interest. Think of it like taking out a business loan or using a credit line—your company gets immediate cash, but it comes with a bill. You maintain full control of your business, but you’re obligated to repay the lender in regular installments, regardless of how well your business performs. Collateral or personal guarantees often back up this kind of financing, so it’s not without risk if things go sideways.

What is Equity Financing?

Equity financing, on the other hand, is about trading a piece of your business for funds. Instead of loans, you invite investors to buy ownership stakes. Angel investors, venture capitalists, or even friends and family might become your new business partners. You don’t have to worry about repayment schedules, but you do give up a slice of future profits and decision-making power.

In short, one path keeps your ownership intact but comes with payback pressure, while the other offers breathing room on repayment but requires sharing your company’s future.

Understanding these two approaches lays the groundwork for exploring the biggest contrasts between them, including who holds the reins and what’s at stake when your business evolves.

Key Differences Between Debt and Equity Financing

Ownership and Control

Raising money through debt keeps all ownership in your hands. Lenders give you cash, expecting regular payments, but they never claim a piece of your business or a say in its decisions. By contrast, equity financing hands investors a slice of the pie. Accepting their funds means sharing future profits and often inviting them into the decision-making circle. This can reshape your business’s direction—sometimes with helpful expertise, sometimes with unexpected opinions.

Repayment and Costs

Debt financing has a straightforward price tag: interest. Every loan comes with a schedule and clear costs—miss payments, and you face penalties. Fortunately, pay on time, and the arrangement ends cleanly after the debt is repaid. Equity, however, technically costs nothing up front and no fixed payments. But the real price is a share of potential profits: as your company grows, your investors’ payouts do too. Over time, that can dwarf what you’d pay in interest on a loan.

Risk and Impact on Business

Taking on debt means betting you’ll have steady cashflow to keep up with payments, no matter how your business actually performs. Fail to meet obligations, and your assets—or business—can be at risk. Equity, on the other hand, offers more breathing room if cash is tight, since there’s nothing to repay on a rigid schedule. But it also means not all rewards are yours alone—and you may need to align your vision with new partners.

Understanding these fundamental differences makes it easier to weigh the financial and personal impact of each path. Next, let’s examine the upsides and trade-offs you’ll face with both debt and equity options, so you can make a choice that truly fits your goals.

Pros and Cons at a Glance

Debt Financing: Benefits and Drawbacks

Equity Financing: Benefits and Drawbacks

Both approaches put specific demands and benefits on the table. As you consider these trade-offs, it helps to know exactly who’s offering funds and what that might look like in practice. Let’s look at the common sources for each route to see what fits your needs.

Common Sources of Debt and Equity Funding

Typical Debt Sources

Banks and credit unions are the classic places businesses turn when they need to borrow. Whether it’s a straightforward term loan or a flexible line of credit, these institutions offer funding with clear repayment terms. For smaller sums or fast decisions, online lenders and peer-to-peer lending platforms have become increasingly popular, often providing quick access to cash without the paperwork marathon.

Another widely used option is equipment financing. Here, the machine, vehicle, or tool you need serves as collateral for the loan, often making it easier to qualify even if your business is young. If your startup has a track record or strong invoices, you might also consider invoice financing. With this approach, a lender advances you money against outstanding invoices, easing cash flow pressure as you wait for customers to pay up.

Credit cards, although sometimes risky due to high interest, can also serve as a short-term way to cover costs, especially for daily expenses or minor purchases. For companies with ambitious growth plans, government-backed small business loans can bring lower interest rates and friendlier terms, though they require patience and paperwork.

Popular Equity Sources

Angel investors are often the first external equity backers for young companies. These individuals invest their own money, typically in exchange for a slice of ownership and maybe a seat at your table as an advisor. If you need more capital and support, venture capital firms step in next, bringing both deeper pockets and high expectations for rapid growth.

For those willing to share their story widely, crowdfunding platforms allow businesses to raise money from the general public, often in exchange for early access to products or company shares. Another route is bringing on strategic partners—people or companies with industry know-how who offer capital in return for equity plus their expertise.

Friends and family sometimes fill the funding gap when conventional sources aren’t an option. While this arrangement can be less formal, clear agreements and open communication are essential to avoid straining relationships.

With so many funding choices out there, understanding where to look is only half the journey. Next, let’s see how these financing options work out in the real world through practical examples.

Real-World Examples: How Each Option Plays Out

Understanding theory is one thing, but nothing beats seeing how financing decisions unfold for actual businesses. Let’s look at a couple of stories where choosing debt or equity made all the difference.

Debt in Action: “Joe’s Gym” and the Power of Leverage

Joe had a thriving neighborhood gym but needed $100,000 to expand. He could have invited an investor, but didn’t want to give up any part of his business. Instead, Joe took out a five-year bank loan with fixed monthly payments. The bank didn’t ask for a say in gym operations—just proof he could make payments. The loan gave Joe full control. Once paid off, the gym’s extra revenue went straight into Joe’s pocket. The flip side? If business had dipped, Joe would still have owed those payments—no matter what.

Equity Example: A Tech Startup’s Rocket Boost

A group of engineers launched a mobile app with big dreams but modest funds. They landed a $500,000 investment from a venture capital firm in exchange for 20% ownership. There were no loan payments, and cash could fuel aggressive growth. The downside? The VC firm wanted input on key decisions and a share of any future profits. When the app went viral, the founders weren’t sole owners anymore, but the company’s meteoric rise likely wouldn’t have happened without that early investment.

Choosing What Fits

Whether you borrow from a lender or invite an investor, the impact shapes everything from your business’s growth speed to who calls the shots. It’s not about right or wrong—it’s about what suits your ambitions and risk tolerance. Now that you’ve seen financing in action, let’s map out how you can apply these lessons to your own situation.

Which Financing Option Fits Your Business?

Factors to Consider Before Deciding

No two businesses share the same balance sheet, ambitions, or appetite for risk. Choosing between debt and equity isn’t simply a numbers game—it depends on your growth stage, industry, and long-term vision. For instance, a tech startup aiming for exponential growth may thrive on equity partners who bring not just money, but advice and networks. A local bakery, on the other hand, could benefit from a manageable loan that keeps ownership firmly in the family’s hands.

Your current cash flow matters. If monthly income is steady, taking on a loan with predictable payments might be straightforward. If revenue swings widely each season, you may find more breathing room with equity funding that doesn’t require regular repayments.

Also, consider how much control you’re willing to share. Debt puts you on the hook for repayment but leaves business decisions up to you. Equity means giving up a portion of ownership—possibly inviting new voices and viewpoints into your boardroom.

Questions to Ask Yourself

Before signing on any dotted line, reflect on these points:

Take some time to map out your non-negotiables. Your answers will point towards the approach best aligned with your business DNA. But what if neither path alone feels quite right? In the next section, you’ll discover how some entrepreneurs combine both strategies to build a more flexible financial foundation.

Blending Debt and Equity: Is a Mix Right for You?

Why choose just one path when you don’t have to? Many businesses find that a “hybrid” funding strategy—combining both debt and equity—unlocks more flexibility than sticking to a single option. With a balanced mix, you harness the strengths of each approach while tempering the risks.

Imagine you’re launching a new product. Taking on some debt allows you to fund inventory or equipment while retaining full ownership. But to attract experienced partners or tap into networks, you might offer a slice of equity. Mixing both means you can lever up when interest rates are low, then swing toward equity to avoid heavy repayments when cash is tight.

There’s no “one size fits all” formula for how much debt or equity to use—it depends on where your company stands in its life cycle, your appetite for risk, what future investors might expect, and how much control you’re willing to share. Many startups start equity-heavy, shifting toward debt later as revenues become reliable. Others alternate, depending on markets and needs.

Savvy founders often use convertible notes or SAFE agreements—tools that bridge debt and equity. These flexible instruments offer short-term runway with the option to convert the debt to equity down the road, giving both the founder and investor more choices as the business matures.

Before mixing and matching, map your goals and growth stages. Talk openly with stakeholders, and keep your long-term vision in focus. Balancing sources can be a tightrope act, but get it right and you position your business to weather changes, raise your profile, and fuel growth on your own terms.

As you weigh your options, a side-by-side snapshot of debt and equity can help clarify the trade-offs and guide your financing journey.

Summary Table: Debt vs Equity Financing Comparison

Loans, bonds, and credit lines from banks or other lenders.

Investment from individuals, venture capitalists, or public markets.

No ownership stake given away; you keep full control.

Investors receive partial ownership and may gain voting rights.

Principal plus interest, usually via fixed payments.

No repayment schedule—investors are paid through dividends or share value growth.

Interest expenses; may require collateral.

Sharing future profits and decision-making.

Missed payments can result in penalties or asset loss.

No obligation to repay if profits are low, but lose some control.

Affects credit rating; increases liabilities.

No debt added; company balance sheet stays lighter.

Can be faster to secure, especially with good credit.

Often slower due to due diligence and negotiation.

Businesses with steady revenue and a need to retain control.

Startups or ventures aiming for rapid growth without upfront repayment burden.

With this side-by-side breakdown, it’s easier to see which financing approach aligns with your business’s needs, resources, and growth plans. Now, let’s delve into some practical tips to help you make a confident decision for your company’s future.