How to Calculate Burn Rate: Step-by-Step for Startups and Small Businesses

If you’re running a startup or a small business, keeping an eye on your burn rate could be the difference between thriving and running out of funds. Burn rate is simply how fast you’re spending cash each month, and it’s one of the first numbers investors, founders, and even employees want to know. According to CB Insights, about 38% of startups fail because they run out of money. Knowing your burn rate helps you understand how long your current funds will last—your cash runway—so you can plan ahead, make smarter decisions, and avoid surprises.

This guide will break down how to calculate burn rate in straightforward steps, using real examples and simple formulas. Whether you’re new to business finances or just want a quick refresher, you’ll find out how burn rate works, why it matters, and what your numbers are really telling you. Let’s get started with the basics.

Burn Rate Explained Simply

Burn Rate in Everyday Business Terms

Burn rate is the pace at which a business spends its cash. Imagine a leaky bucket filled with water: if your income is less than your spending, water escapes faster than you fill it. Burn rate tells you how quickly the cash inside the bucket will disappear if nothing changes.

If your startup spends $10,000 each month and brings in $2,000, your monthly burn rate is $8,000—the net amount you lose. This number helps you see how long your company can operate before the bucket runs dry.

Why Burn Rate Matters for Your Survival

Knowing your burn rate shows you how much time you have to find customers, secure funding, or lower costs before you’re out of cash. A high burn rate means you could be heading for danger quickly; a low burn rate buys you more time and options.

Burn rate acts as an early warning signal, showing you when you need to adjust spending or boost income. It keeps you from guessing about your startup’s future, so you can steer with confidence instead of hope.

Now that you understand what burn rate is and why it’s vital, let’s untangle the different types—because not all burn rates are created equal.

Types of Burn Rate: Gross vs. Net

What Is Gross Burn Rate?

Gross burn rate is all about cash out. It shows how much money your business spends each month, regardless of how much you bring in. Imagine a bucket with a hole—gross burn rate is the water leaking out, ignoring any water you pour back in. It captures total expenses like salaries, rent, software subscriptions, and supplier payments. The only focus is what leaves your bank account.

What Is Net Burn Rate?

Net burn rate tells the bigger story: how much money you actually lose each month. It takes your total outgoing cash and subtracts any revenue you collect. This way, you see your real cash loss for the month. Using the same leaky bucket example, net burn rate measures how fast the bucket is emptying after refilling it with the revenue you’ve earned. If your net burn is $10,000, your bank balance shrinks by that amount each month.

Which Should You Track?

Both have their uses. Gross burn rate gives a reality check on costs—critical when you need to cut spending fast. Net burn rate reveals how long your cash will last, considering income. If you want a true picture of survival time or runway, net burn rate matters more. But if you’re chasing aggressive growth or facing a sales slump, keep an eye on both to avoid surprises.

Next, let’s break down how to do these calculations step by step with simple formulas and real-world examples, so you can easily spot warning signs and make confident decisions.

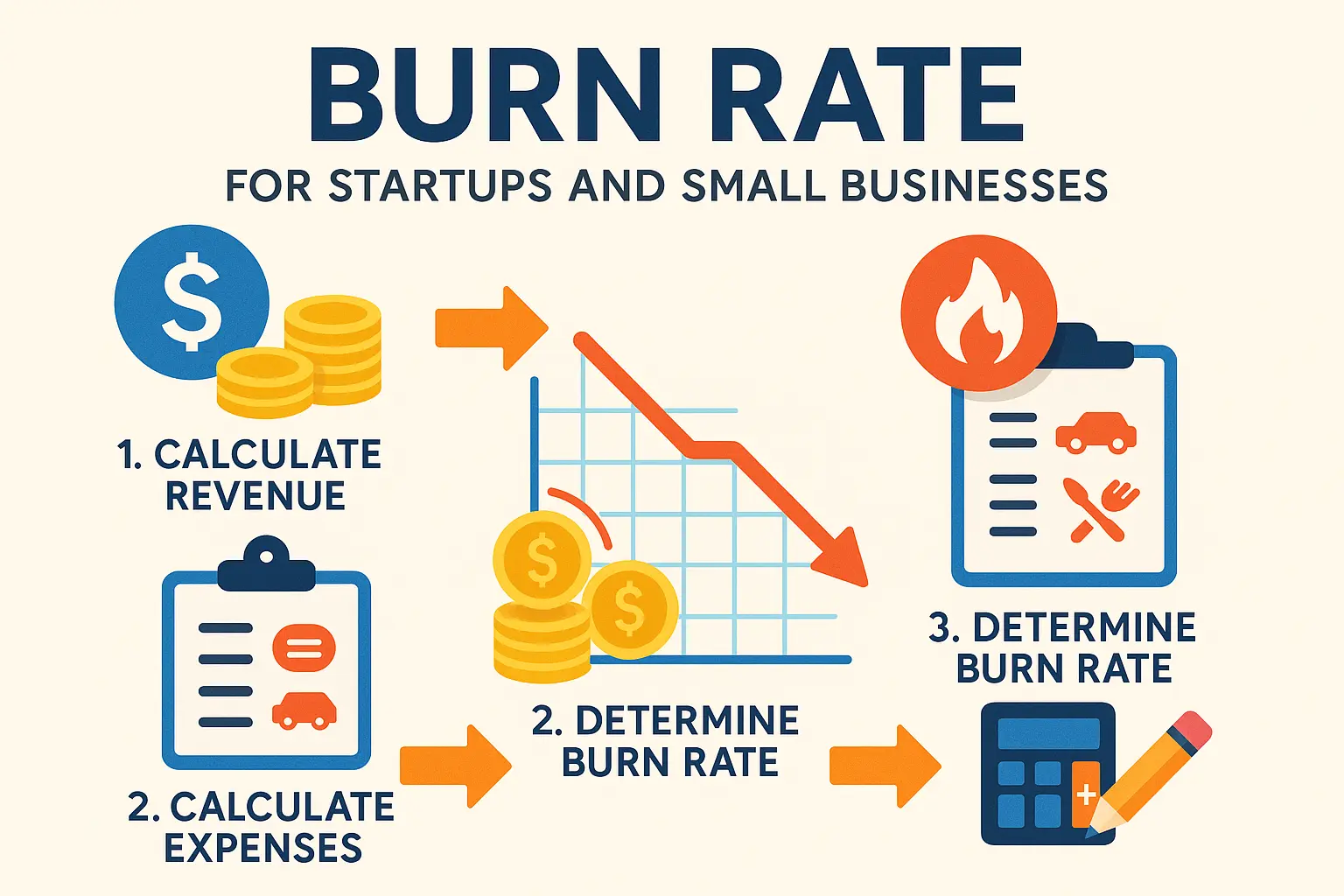

How to Calculate Burn Rate

Formulas with Simple Examples

Calculating burn rate is about knowing how much money your business loses during a set period, usually each month. The most basic formula is:

Burn Rate = (Starting Cash – Ending Cash) / Number of Months

For example, if your business had $50,000 at the start of January and $35,000 at the end of March, the calculation would be:

Burn Rate = ($50,000 – $35,000) / 3 = $5,000 per month

This tells you that, on average, you’re spending $5,000 more than you’re bringing in every month. You can adapt this formula for shorter or longer timeframes.

Monthly vs. Weekly Calculations

While most startups look at monthly burn rate, you can choose a shorter window if you want a sharper view of cash movement. Calculating your weekly burn rate just involves changing the timeframe in the same formula:

Weekly Burn Rate = (Starting Cash – Ending Cash) / Number of Weeks

This can make sense if your business is new, changes rapidly, or needs more frequent check-ins.

Sample Calculation for a Startup

Let’s say your startup raised $120,000 and started spending in January. By the end of April, your balance is $88,000. Subtract the ending cash from what you started with, then divide by four months:

Burn Rate = ($120,000 – $88,000) / 4 = $8,000 per month

This means you’re “burning” $8,000 each month. With $88,000 left, you can use this number to estimate how many months you have before running out—if nothing changes.

Now that you’ve worked out your burn rate, it’s time to see how this number reveals the lifespan of your business cash and what it means for your planning ahead.

Burn Rate and Cash Runway: How They’re Linked

Runway Calculation with Burn Rate

Think of your company’s cash runway as the time until you run out of money, assuming nothing changes. Burn rate is the key variable in this equation. Specifically, your cash runway is calculated by dividing your available cash by your net monthly burn rate:

Cash Runway (months) = Total Cash / Net Monthly Burn Rate

For example, if you have $120,000 in the bank and a net burn rate of $20,000 each month, your runway is 6 months. Simple math but powerful insight—it tells you exactly how much time you have to reach profitability, secure new funding, or adjust operations. Remember, this number assumes your expenses and income stay the same—any major change can lengthen or shorten your runway fast.

What a ‘Good’ Runway Looks Like

How much runway should you have? There’s no perfect answer, but most startups try to keep at least 12 months of runway. This cushion allows for unpredictable delays in product development or fundraising. If your runway dips below six months, it’s a red flag—either costs need to come down or new money must come in quickly. Conversely, keeping too much idle cash can mean missed opportunities for growth.

Finding your ideal runway depends on your industry, fundraising cycles, and business model. Take time to reassess whenever your burn rate changes or when your goals shift. A healthy runway isn’t just about survival—it’s about having time to make the smartest moves for your company’s future.

Once you understand the story your numbers are telling about runway and burn rate, the next step is learning what those numbers mean for your business decisions and how to spot trouble before it hits.

Interpreting Burn Rate: What Your Numbers Say

High Burn Rate: Risks and Signals

If your burn rate is high, it means your cash is leaving the bank faster than it’s coming in. For startups and small businesses, a high burn rate can feel like running with your shoelaces untied—all energy, but one misstep could lead to disaster. It often signals that expenses, such as payroll, marketing campaigns, or inventory purchases, are outweighing the money you bring in.

When the burn rate spikes, two big warnings flash: your runway shortens, and fundraising pressure grows. You may need to secure investment earlier than planned or scramble to cut back on spending. Sometimes, a high burn rate is part of a growth plan—like hiring a bigger team before launching a product—but it must be paired with a clear path to increased revenue or funding. If not, you risk running out of cash long before your big goals are within reach.

Low Burn Rate: Pros and Cons

A low burn rate stretches your runway, giving your business more time to find its footing, test new products, or weather unexpected storms. This discipline is especially valuable for startups with uncertain sales cycles or those bootstrapping without external funding. It can help you stay in control—making decisions from a place of strength, not desperation.

But ultra-low burn rates aren’t always a win. Being overly cautious about spending may slow down growth or cause you to miss opportunities. Delaying key hires, holding off on marketing, or not investing in better technology can let competitors pass you by. The trick is finding a balance: enough restraint to survive, but enough investment to move forward.

The story your burn rate tells isn’t just about the money spent—it’s about the kind of business you’re building and how quickly you plan to get there. Once you understand what your current numbers mean, the next step is shaping them into the ones you want. Let’s look at how to influence your burn rate so it matches your goals and strategy.

Ready to Take Control of Your Burn Rate?

Knowing your burn rate is one thing—using it to steer your business is another. Don’t let guesswork put your vision at risk. Get hands-on: run the numbers, check your balances, and make decisions powered by real data. Give yourself the insight needed to adjust early rather than scramble later.

Whether you’re burning through cash fast or holding your ground, the right approach can change your game. Now, it’s not just about knowing the numbers—it’s time to improve them. Let’s dig into practical moves that can help you extend your runway and strengthen your bottom line next.

How to Improve Burn Rate Effectively

Cutting Unnecessary Costs (with Examples)

Start by reviewing your biggest expenses. Look for subscriptions you rarely use, software licenses that aren’t essential, or advertising channels that don’t convert. For example, many startups pay for multiple project management tools but rely on only one—cancel or downgrade the rest. Renegotiate contracts with vendors or switch to more affordable options. If you rent unused office space, consider subleasing it to others. Small actions like shifting to open-source alternatives or buying supplies in bulk instead of piecemeal can quickly add up.

Boosting Revenue Streams

Increasing income can improve your burn rate faster than cuts alone. Spot overlooked sources: Can you upsell existing customers, offer premium add-ons, or launch a referral program? If you have idle equipment or skills, rent them out or start a pilot service. Collaborate with partners on joint offers or bundle products to move more inventory. Think about holding a short-term promotion to bring in quick cash and gauge which offers draw the most attention.

Tools and Tips for Tracking

Manual tracking in spreadsheets is where most founders start, but automation saves time and catches leaks you’d otherwise miss. Use tools like QuickBooks or Xero to categorize expenses, track recurring charges, and generate clear visual reports. Set weekly “check-ins” to review actual spend versus projections. Alerts for sudden budget spikes can catch mistakes early. Connecting your bank feeds to your tracking software means fewer manual errors and better visibility.

Once you’re actively managing your burn rate, the next step is knowing what actually counts toward it, how often to check in, and spotting warning signs before they become problems.

FAQs on Burn Rate Calculation

What expenses count toward burn rate?

Burn rate focuses on all the cash your business spends, not just the bills you pay every month. This includes payroll, rent, marketing, insurance, software subscriptions, supplier payments, and any operational outflows. Ignore any non-cash expenses like depreciation or stock compensation—these don’t actually leave your bank account, so they don’t affect your burn rate.

How often should I recalculate?

If you’re running a startup or small business, update your burn rate monthly. As your business grows or if your expenses are volatile, consider checking in every couple of weeks for a sharper pulse. Recalculation is key when your spending habits (like new hires or launching campaigns) or income streams change suddenly.

When should I worry about my burn rate?

If your burn rate eats into your cash runway faster than planned, or you see your bank balance shrinking with no revenue boost in sight, it’s time to take notice. A spike without a solid strategy—whether it’s due to unexpected costs or falling sales—means you’ll need to act quickly to avoid trouble down the line.

Now that these common questions are covered, let’s look at practical moves you can make to keep your cash flow in check and strengthen your financial safety net.